Ind AS Consulting Services

Ind-AS has been made applicable from the financial year 2016–2017. At Azebons, we specialize in supporting corporates through a seamless transition to this new statutory framework.

1. Ind AS implementation road map

| Phase I | Phase II | Voluntary adoption | |

| Year of adoption | FY 2016 – 17 | FY 2017 – 18 | FY 2015 -16 or thereafter |

| Comparative year | FY 2015 – 16 | FY 2016 – 17 | FY 2014 – 15 or thereafter |

| Covered companies | |||

| (a) Listed companies | All companies with net worth >= INR500 crores | All companies listed or in the process of being listed | Any company could voluntarily adopt Ind AS |

| (b) Unlisted companies | All companies with net worth >= INR500 crores | Companies having a net worth >= INR250 crores | |

| (c) Group companies | Applicable to holding, subsidiaries, joint ventures, or associates of companies covered in (a) and (b) above. |

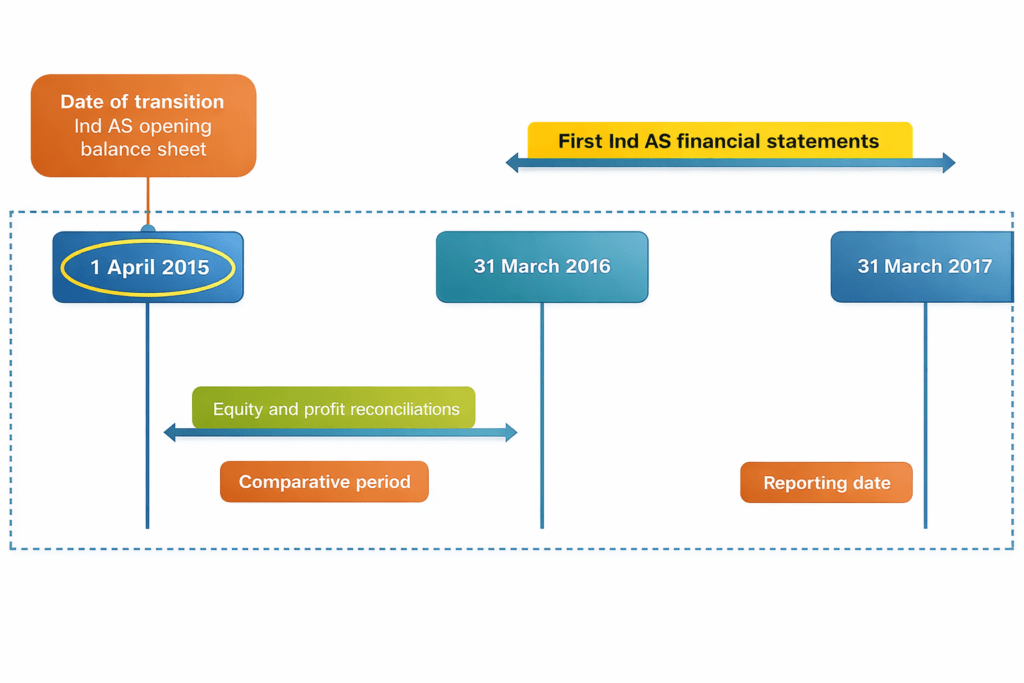

2. Various stages under Ind-AS implementation:

3. Scope of work

Our comprehensive approach is designed to deliver an end-to-end solution, ensuring a smooth transition from existing accounting practices to Indian Accounting Standards (Ind AS), starting from Financial Year 2016–17.

The scope of work includes:

- Identification of key differences between current Indian GAAP and Ind AS, including accounting and reporting variations

- Evaluation and selection of applicable exemptions under Ind AS 101

- Impact assessment across various business components, including financials and IT systems

- Development of a detailed implementation roadmap based on the impact analysis

- Assistance in preparing Ind AS-compliant financial statements for the transition date, comparative period, and reporting period

- Support in preparing the opening balance sheet as of 1st April 2016

- Assistance in preparing financial statements for the comparative period (FY 2016–17) and reporting period (FY 2017–18)

- Conducting training sessions to facilitate knowledge transfer and help teams understand post-transition changes

- Support during statutory audits, including discussions with auditors to address and resolve any differences in interpretation related to Ind AS transition